Ever since the housing bubble burst, the American public has been bombarded by predictions of all sorts. Some have included assertions that the real estate market has bottomed out, while others issue dire warnings that it will sink still lower. Accompanying these negative reports, however, there have usually been optimistic voices insisting that the market is actually improving. And perhaps it finally is. Dubious? Read on…

According to a report issued recently by the Demand Institute, 2012 is the year of the housing bottom. The report states, “The double-digit increases in U.S. housing prices over the first half of the past decade proved unsustainable. But the freefall is over. The point has been reached where housing prices will start to climb, albeit at single-digit rates in most markets over the next five years.”

In addition, Douglas C. Yearley, Jr., CEO of Toll Brothers,says: "It appears that the housing market has moved into a new and stronger phase of recovery as we have experienced broad-based improvement across most of our regions over the past six months. The spring selling season has been the most robust and sustained since the downturn began.”

Numerous recently published articles discuss various stages of a housing market recovery. Some describe a 3-step process, some 5, and others 7, but all agree that the signs of an upswing are currently here. Visit Zip Realty, Seeking Alpha, and GMO for in-depth explanations and analyses of these stages.

Moreover, the Wall Street Daily touts 11 positive indicators that point to the beginning of a real estate turnaround. Among those featured are rising housing starts, declining inventory, growing consumer confidence, spiking rental costs, increasing prices of homes, and rebounding existing home sales.

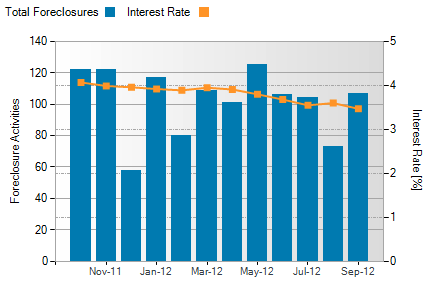

If you are considering buying or selling a home, this may well be a good time to do so. Interest rates won’t get much lower, prices seem to be stabilizing, and houses are more affordable than they’ve been in a decade. Why wait any longer?

Lets look at the statistics in our local real estate market for September 2012.

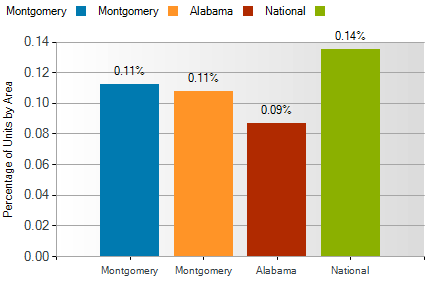

Midtown Montgomery real estate sales statistics for September show the number of homes sold decreased by 16% when compared to September 2011. The average sales price decreased by 5% to $131,321 during the same period. The median sales prices decreased by 3%, and market times decreased by 35% or 60 days. The highest selling home price decreased by 14%, and the lowest selling home price increased by 100%.

|

Midtown Montgomery |

Sept 2012 |

Sept 2011 |

|

Homes Sold |

21 |

25 |

|

Average Selling Price |

$ 131,321 |

$ 138,288 |

|

Median Selling Price |

$ 122,500 |

$ 126,500 |

|

Days On The Market |

114 |

174 |

|

Highest Selling Price |

$ 367,500 |

$ 425,000 |

|

Lowest Selling Price |

$ 25,500 |

$1 |

For the latest Midtown Montgomery real estate market conditions in your area, please call me at 800-HAT-LADY or visit HomesForSaleInMontgomeryAlabama.com.

Information is provided by the Montgomery Area Association of Realtors and is deemed accurate but not guaranteed.

.jpg)

Results from Fannie Mae’s September

Results from Fannie Mae’s September .jpg)

Enjoy It Now

Enjoy It Now Tonight is the night

Tonight is the night