Montgomery AL Foreclosure Trends - July 2011

There were 1,069 Montgomery AL foreclosure homes for sale with 92 new foreclosures in July 2011. The average selling price of a Montgomery AL home was $146,582 and the average foreclosure selling price was $76,628 a $69,953 savings, according to RealtyTrac.com.

Montgomery AL Foreclosure Activity and 30 Year Interest Rate

Montgomery interest rates averaged 4.55% in July while the number of foreclosed homes decreased from 100 in June to 92 in July.

Foreclosure activity is based on the total number of properties that receive foreclosure filings – default notice, foreclosure auction notice or bank repossession – each month. Interest rate is based on the average 30-year fixed rate from Freddie Mac Primary Mortgage Market Survey.

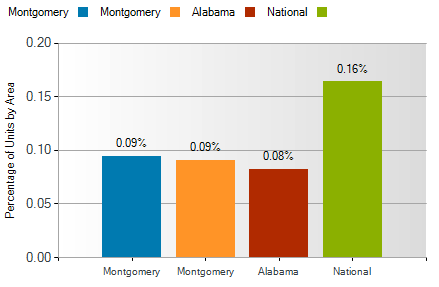

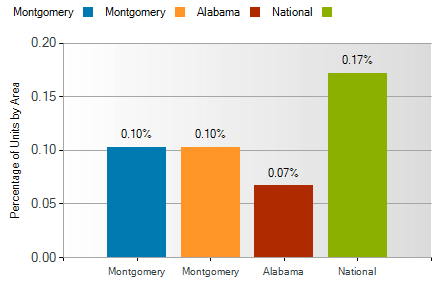

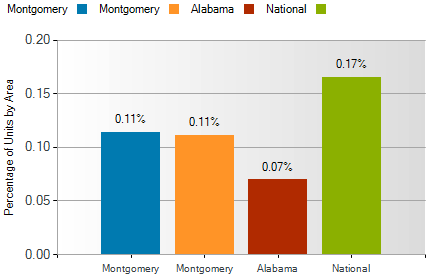

Montgomery AL Foreclosure Geographical Comparison

Montgomery AL foreclosure activity was 0.07% lower than national statistics. 0.01% higher than Alabama and the same as Montgomery County statistics for the month of July.

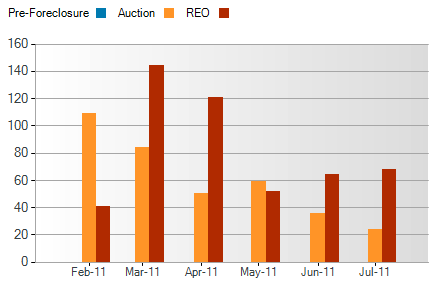

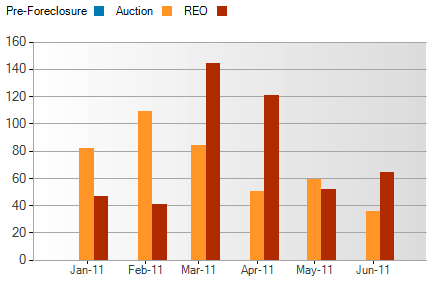

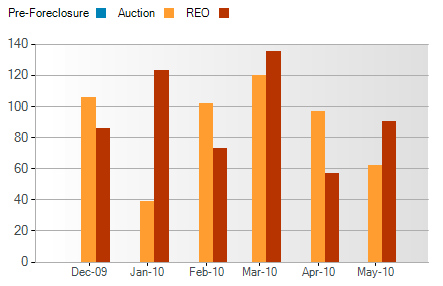

Montgomery AL Foreclosure Activity by Month

The number of Bank-Owned properties increased from 64 homes in June to 68 in July. The number of Auctions decreased from 36 to 24. There is a 6-month falling trend.

Are you or someone you know behind on mortgage payments and facing a Montgomery foreclosure? You do have options. A short sale may be the answer to saving you, your family and your home. I am a Certified Distressed Property Expert (CDPE) with specialized training in helping families avoid foreclosure. Give me a call for a private consultation.

who is experienced in new home sales. A strong realtor negotiating on your behalf can save you thousands!

who is experienced in new home sales. A strong realtor negotiating on your behalf can save you thousands! A reverse mortgage is a special type of home loan based on age, equity, interest rates, and the

A reverse mortgage is a special type of home loan based on age, equity, interest rates, and the