If you’re a seller of a Montgomery home you need to understand the complexities of negotiating. This is particularly true if you are attempting to sell your home by yourself. This is known as a “for sale by owner” or FSBO.

Most people understand that selling a home is complicated. But just about the least understood component of being a seller is the need to do a lot of negotiating. Even if you are working with a Realtor it is good to know what is going on, often behind the scenes. Why? So you have an appreciation of what the Realtor is doing for you.

Most people understand that selling a home is complicated. But just about the least understood component of being a seller is the need to do a lot of negotiating. Even if you are working with a Realtor it is good to know what is going on, often behind the scenes. Why? So you have an appreciation of what the Realtor is doing for you.

Here are just a few of the types of negotiations you need to be ready to deal with…

- The buyer’s agent whose sole responsibility it is to protect the best interest of the buyer, not yours.

- The buyer who wants the best deal possible from you.

- The home inspection company which is working for the buyer and almost always finds problems with the property for sale.

- The termite company if there are challenges by the buyer.

- The buyer’s lender if the structure of the financing requires the seller’s participation.

- The appraiser if there is a question of value.

- The title company if there are any challenges with permits, certificates of occupancy, or the survey.

- The municipal government if there a problems with permits or certificate of occupancy.

- The survey company if there any discrepancies or challenges.

Every one of the above participants in a real estate transaction has special interests and specialized knowledge about a different component in the sales process. Each one has to be negotiated with on some level to make sure the sale gets to closing smoothly.

It takes a lot of skill to understand everyone’s interests and how those interests fit into the bigger picture. Some of their interests and intertwined, and some are very specific to a given specialty. Some of the interests are very objective and others are very subjective and emotional.

In addition to all of that, your emotions as the seller tend to run high. It is extremely difficult to remain calm and objective when dealing with other people over the sale of your Montgomery home. That is because you are not just selling a house and a property…you are selling the home you and your family have lived in. It’s personal.

The primary message is to be very careful about making a decision to go the FSBO route and be very selective when deciding on a Realtor to be your agent of negotiation.

Ready to sell? Click here for the 7 Essential Steps to Selling Success!

Sandra Nickel and the Hat Team have distinguished themselves as leaders in the Montgomery AL real estate market. Sandra assists buyers looking for Montgomery real estate for sale and aggressively markets Montgomery AL homes for sale. Sandra is also an expert in helping families avoid foreclosure through short sales and is committed to helping families in financial hardship find options. For more information you can visit AvoidForeclosureMontgomery.com.

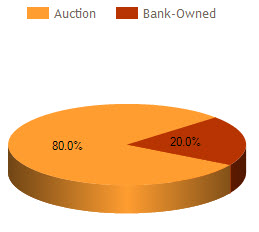

Interested in buying a bank-owned home? Get bank-owned listings alerts FREE!

You can reach Sandra by filling out the online contact form below or give her a call anytime.

The 2013 standard deduction for a married couple filing jointly is $12,200 and $6,100 for a single taxpayer. It doesn’t require any proof of actual expense and has no requirement for home ownership.

The 2013 standard deduction for a married couple filing jointly is $12,200 and $6,100 for a single taxpayer. It doesn’t require any proof of actual expense and has no requirement for home ownership.

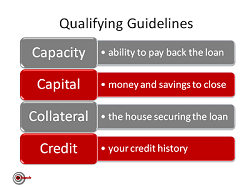

The Qualified Mortgage Rule came into effect on January 14, 2014 as one of the results to the Dodd Frank Reform Act to protect consumers from predatory lending practices. This will affect the underwriting standards that the majority of lenders will use to qualify borrowers.

The Qualified Mortgage Rule came into effect on January 14, 2014 as one of the results to the Dodd Frank Reform Act to protect consumers from predatory lending practices. This will affect the underwriting standards that the majority of lenders will use to qualify borrowers.