Montgomery AL Real Estate For Sale: 341 Winthrop Ct

Montgomery Homes For Sale:

341 Winthrop Ct, Montgomery, AL 36104

MLS #315478

Stunning Renovation in Garden District!

.jpg)

Incredible Craftsman style renovation on one of the Garden Districts best kept streets. Beautiful reclaimed columned mantle greets you upon entry into large formal living room with built in book cases. Gas logs for cozy nights by fireplace. Huge formal dining adjoins with widows on two sides with lots of sunlight. Three nice sized bedrooms and refinished floors will be the perfect complement to your furnishings. You will enjoy 18 inch hard tile flooring in kitchen as well as almost new appliances, cabinets, granite counter-tops, tile back splash, flush can lighting, bead board wainscoting and ceiling. Wonderful eat-in area off kitchen is conveniently located next to French doors to covered area perfect for cook outs. Back deck has commanding view of treed and private rear yard. Stunning main bathroom will wow you with nice fixtures, hard tile floor, vaulted ceiling, jetted tub and unique antique vanity with double sinks. Almost forgot to mention a real front porch for sitting and watching neighbors pass. Current owner has added a spacious detached out building that matches house for all your outdoor and yard things. Seize the opportunity to buy that rare vintage home with all the new things you would want in an old one. One year warranty included. Easy to show! Give us or your favorite agent a call today!

Marketed by Montgomery Alabama Realtor Sandra Nickel, Sandra Nickel Hat Team.

There are three primary sources for credit scores in the US:

There are three primary sources for credit scores in the US:

.jpg)

1. Spending the maximum amount on a mortgage a lender will loan.

1. Spending the maximum amount on a mortgage a lender will loan.

While the borrower and the property affect the rate and terms that a lender may offer, it is not to be said that all lenders will offer the same terms and rates to the same buyer. Credit score, home location, home price and loan amount, down payment, loan term, interest rate type and loan type all affect the interest rate but different lenders can interpret this information differently.

While the borrower and the property affect the rate and terms that a lender may offer, it is not to be said that all lenders will offer the same terms and rates to the same buyer. Credit score, home location, home price and loan amount, down payment, loan term, interest rate type and loan type all affect the interest rate but different lenders can interpret this information differently.

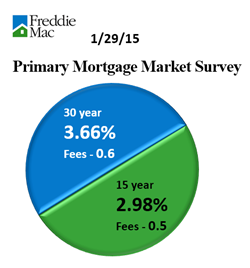

Does this hold true for you?

Does this hold true for you?.jpg)