Montgomery AL Foreclosure Trends - February 2012

There were 874 Montgomery AL foreclosure homes for sale with 1 in every 1,181 housing units receiving a foreclosure filing in February 2012. The average selling price of a Montgomery AL home was $97,803 and the average foreclosure selling price was $69,578, a $28,225 savings according to RealtyTrac.com.

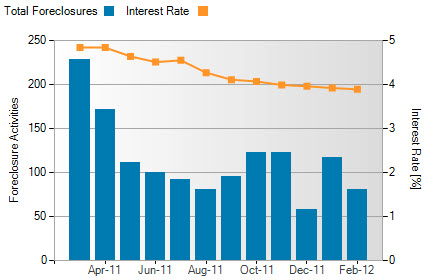

Montgomery AL Foreclosure Activity and 30 Year Interest Rate

Montgomery interest rates averaged 3.89% in February while the number of foreclosed homes dropped from 117 to 80.

Foreclosure activity is based on the total number of properties that receive foreclosure filings – default notice, foreclosure auction notice or bank repossession – each month. Interest rate is based on the average 30-year fixed rate from Freddie Mac Primary Mortgage Market Survey.

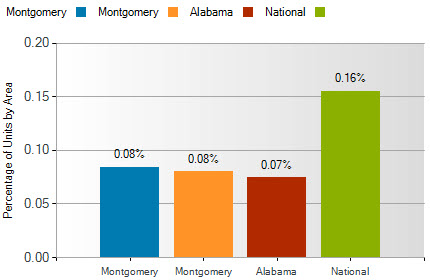

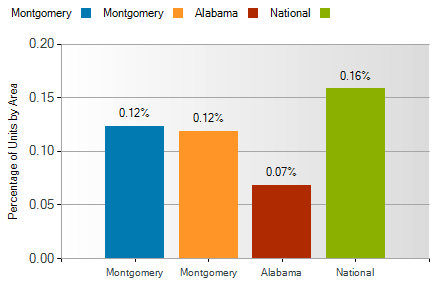

Montgomery AL Foreclosure Geographical Comparison

Montgomery AL foreclosure activity was 0.08% lower than national statistics, 0.01% higher than Alabama and the same as Montgomery County statistics for the month of February 2012.

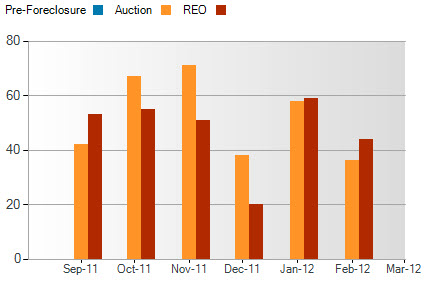

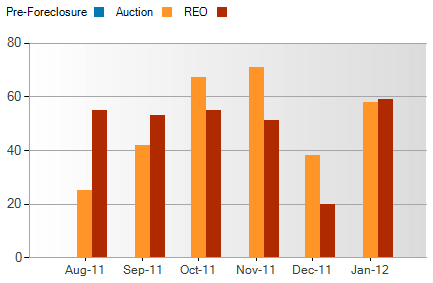

Montgomery AL Foreclosure Activity by Month

The number of Bank-Owned properties decreased from 59 homes in January to 44 in February. The number of Auctions dropped from 58 to 36. There is a 6-month falling trend.

Are you or someone you know behind on mortgage payments and facing a Montgomery foreclosure? You do have options. A short sale may be the answer to saving you, your family and your home. I am a Certified Distressed Property Expert (CDPE) with specialized training in helping families avoid foreclosure. Give me a call for a private consultation.

Search all Montgomery AL Real Estate And Homes For Sale.

Sandra Nickel and the Hat Team have distinguished themselves as leaders in the Montgomery AL real estate market. Sandra assists buyers looking for Montgomery real estate for sale and aggressively markets Montgomery AL homes for sale. Sandra is also an expert in helping families avoid foreclosure through short sales and is committed to helping families in financial hardship find options. For more information you can visit AvoidForeclosureMontgomery.com.

You can reach Sandra by filling out the online contact form below or give her a call anytime.

.jpg)

Unfortunately,

Unfortunately,  TERMS:

TERMS: