Buying is Better than Renting: Here’s Why

With interest rates still relatively low, buying a house right now is less expensive than renting in many places, including Montgomery, AL. Now is a great time to lock into a rate.

Buying is often considered to be financially better than renting over the long run because your mortgage payments build equity in your home, which you will eventually own, while rent only goes toward the upkeep of your home and the pocket of your landlord. That is just one reason buying is better than renting. Here are some others:

- You can do what you want with your property. Making home improvements will be your choice…from colors to paint the walls to light fixtures to types of floors, you won’t need permission from a landlord to make changes.

- Tax benefits. Tax Deductions are a great perk of home ownership.

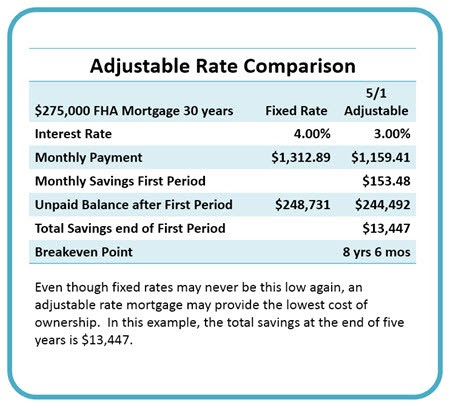

- Stable monthly payments. Rents can go up, but with a fixed-rate mortgage, your monthly payments won’t change.

- Forced savings. Renting might seem less expensive, but would you actually save the money you don’t spend on rent? Since your mortgage payments are building equity in your own home, which you can later sell for profit, it’s like a forced savings.

Using a Rent vs But Calculator you can see how buying is a better financial option right here in Montgomery. For example, after 4 years, the cost of homeownership (down payment, mortgage, taxes, etc.) for a $150,000 home in Montgomery would be $94,094. The total cost to rent the same house for that period would be $52,193. Renting would leave you with $41,901 in your pocket (including the money you didn’t spend on a down payment). So, it looks like renting would be better financially, right? But wait…not so fast. Let’s look at what you gain over the same 4-year period if you buy. After 4 years, your home will have $70,371 in equity. However, if you instead rent and invest your down payment and the other money you save at a 6% return rate, it will earn around $8,351 in 4 years. So, if you look at your gross costs, equity and investment potential, it’s better for you to buy than rent if you plan to live in your home more than 3 years and 3 months.

The bottom line is, if you’ve been thinking about buying a home in the Montgomery area, don’t wait! Start investing your money in your own home vs that of a landlord today!

Contact Sandra Nickel and her Hat Team of professional Realtors at 334-834-1500 and let them help you find your dream house today!

Lenders, like any business, have to make a profit. The cost of acquiring the funds, the operating costs to service and the expected profit margin are easily identified. The variable in pricing is the type of mortgage and the credit worthiness of the borrower.

Lenders, like any business, have to make a profit. The cost of acquiring the funds, the operating costs to service and the expected profit margin are easily identified. The variable in pricing is the type of mortgage and the credit worthiness of the borrower.