Generating Wealth Through Home Ownership

When you purchase a home, you are not only choosing where to live, you are making a financial investment as well. Home equity is the percentage of your home value that you own and with each mortgage payment you make you are contributing to your own financial savings. The goal is to build up as much equity as you can so that when you sell your home, you will make a nice profit! Here are some tips for building home equity:

- Take Out a 15-Year Mortgage Loan - It’s common for people to choose a 30-year mortgage because many believe a 15-year mortgage is out of their budget. However, it can’t hurt to ask your mortgage lender to run the numbers to see if a 15-year mortgage is doable for you. You might be surprised to discover that the shorter term is within reach. Sticking to a budget that allows you to pay off your house in half the time will build equity faster and will certainly pay off in the long run! 32 Hacks for Sticking to Your Budget

- Pay Down the Principal - Build equity faster by paying down your home loan quicker. Even if you don’t have the ability to take out a 15-year mortgage, you can still make extra mortgage payments when you have the means to do so and the difference extra mortgage payments can make toward building equity are huge. If you make just one extra payment toward principal each year, you can potentially pay off your home loan seven or eight years ahead of schedule. There are ways to do this without breaking your budget. For example, you can use a tax refund or a work bonus. Another way to do it is to simply add a small amount to your principal payment each month.

- Make a Larger Down Payment - Depending on your credit standing, you can qualify for a conventional mortgage loan with a down payment as low as 3%, and an FHA loan with a down payment as low as 3.5%. While it’s tempting to buy a house with a low down payment so that you have more cash on hand, the pros of making a larger down payment may outweigh the cons. The larger the down payment, the faster you build equity. The faster you build equity, the more profit you will make should you have to sell your home before paying it off.

- Make Improvements on Your Home - Making home improvements is a good way to add value to your property. It’s important to educate yourself about what home improvements give you the best ROI (return on investment). For example, per Chris Terrill, CEO of HomeAdvisor, “a minor kitchen remodel is one of the best investments homeowners can make.” “Projects including refinishing cabinets, updating the countertops and installing new appliances all provide high return without breaking the bank.” Other home improvements that add value to your property include replacing garage doors, adding a bedroom, updating a bathroom and installing new windows. And don’t underestimate the value of curb appeal! A professionally landscaped yard will not only help with a quick sale; it can also add up to 20% to your home’s value! Which Home Improvements Pay Off?

Owning a home is likely the largest financial investment you will make, and the more equity you acquire, the more wealth you will generate. You can utilize your equity as a nest egg for the future or it can be used as a cash down payment on your next home. Use these tips to build up your savings an enjoy this wonderful perk of home ownership!

If you are in the market to buy or sell a home, let Sandra Nickel and her Hat Team of Professionals assist you with all your real estate needs! Call them today at 334-834-1500!

Photo Credit: achievalife.com

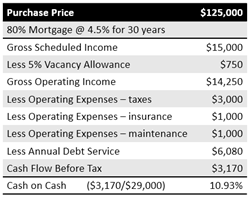

Years ago, real estate investors used to accept negative cash flow buoyed by tax incentives in hopes of making a big payday due to appreciation when they sold it. Today’s investors are focusing on tangible, current results like cash flow and equity build-up.

Years ago, real estate investors used to accept negative cash flow buoyed by tax incentives in hopes of making a big payday due to appreciation when they sold it. Today’s investors are focusing on tangible, current results like cash flow and equity build-up.